Credit Minus the History

Designing a financial product for people the system had already decided to ignore.

■ Telefônica Brasil, trading as Vivo, is a Brazilian telecommunications company and subsidiary of the Spanish Telefónica.

4,000

Applications in first 3 months

8-10%

Conversion rate among applicants

~$90 USD

Average loan (400-500 BRL)

The Starting Point

Pix is Brazil's instant payment system: launched by the Central Bank in 2020, free for individual users, and mandatory across every financial institution in the country, including non-banks. (If you're picturing Zelle, that's a reasonable starting point for translation, though Pix runs across the entire financial system rather than a network of partner banks, and adoption moved far faster.) Within two years, Pix had over 138 million registered users, out of a population of roughly 215 million.

Brazilians adopted it faster than almost any payment technology anywhere in the world. Vivo saw an opportunity: what if their customers could pay in installments through Pix, without needing a credit card to do it?

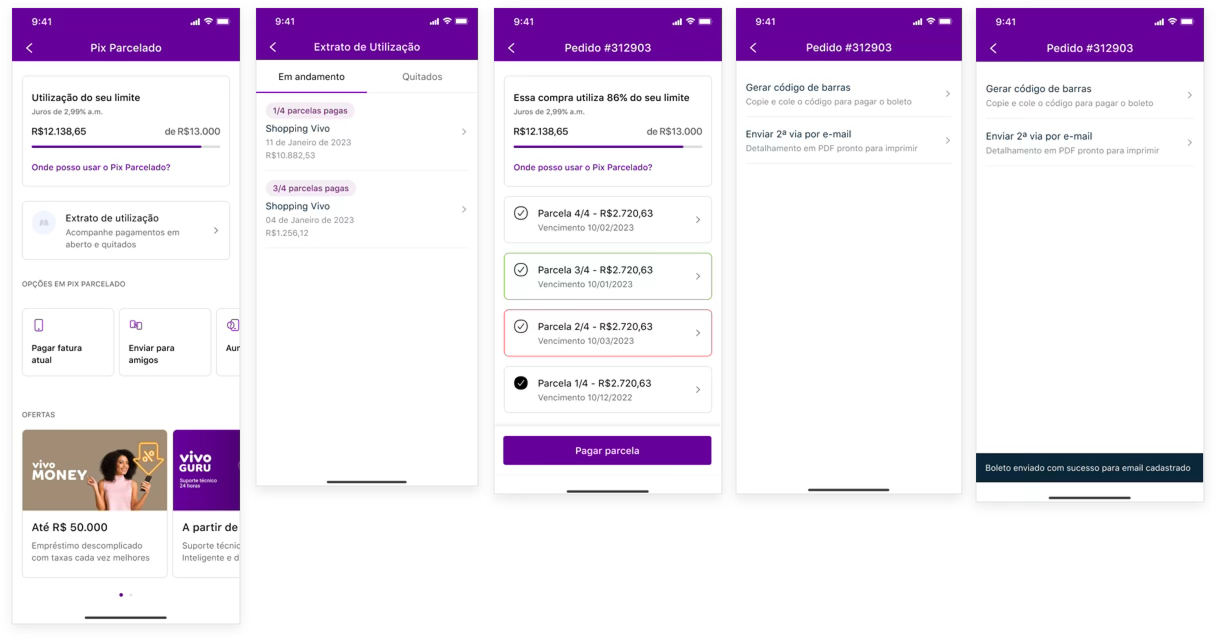

That was the premise behind Parcela Pix. A buy-now-pay-later product built on Brazil's own payment infrastructure, designed to reach the people traditional financial institutions had never bothered designing for.

My Role

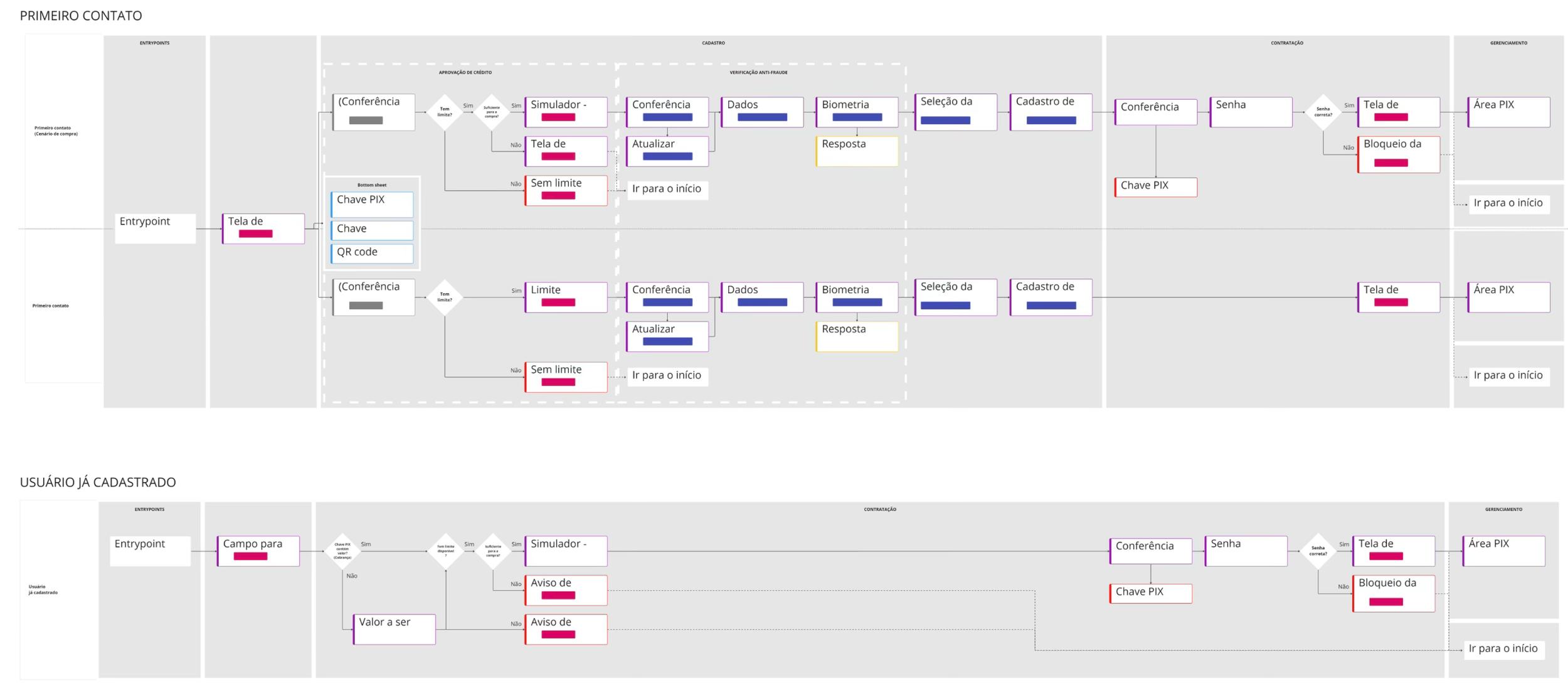

I led the Discover and Definition phases of this project: the work that happens before any screen gets designed. That meant getting clear on who we were actually building for, what we knew, what we were assuming, and what we needed to find out. It's the phase where the important decisions get made, often without anyone realizing it yet.

The challenge wasn't just technical. It was about trust and access. We were designing a credit product for people with little-to-no credit history, which meant the usual eligibility signals didn't apply. Brazil does have credit bureaus, Serasa and Boa Vista, with scores running 0 to 1000. But in practice, what a lender already knows about you as its own customer matters more than the number: keep your salary at a bank and it offers you a better limit than one that has never seen you. Our users weren't risky. They were invisible to institutions that had never held a relationship with them.

Working through an Opportunity Assessment Canvas and iterative stakeholder sessions, we mapped out what we knew for certain, what we were assuming, and where the real risks sat. We defined eligibility criteria that balanced accessibility with sustainability, excluding prepaid customers and recent Vivo joiners, for example, not to be restrictive, but to make the product viable enough to keep running for the people who needed it most.

Vivo had a unique advantage here: the kind of data on their customers that traditional banks simply couldn't see.

What We Were Really Solving For

Here's what surprised us. We had designed with large purchases in mind, the kind of thing you'd traditionally put on a credit card. What users actually did was something different.

Most transactions averaged around 400–500 BRL (roughly $90 USD). Most people chose just 2–4 installments. And around 60% of the money moved wasn't going to merchants at all — it was going to friends and family.

Personal payments. Informal support networks. The kind of financial behavior that the formal system has never had a clean category for.

That finding reframed the product entirely. Parcela Pix wasn't primarily a shopping tool. It was a way for people to manage the financial texture of everyday life: helping a family member, splitting something with a friend, in a way that was structured and manageable rather than stressful.

What the Research Revealed

Parcela Pix launched in May 2024. Within three months it received over 4,000 applications with a conversion rate of 8–10%. Not because we built something flashy, but because we spent the early phases asking the right questions about who we were designing for and what they actually needed. The discovery work shaped everything that came after it. I've often found that to be the case.

The Outcome

The Market We Were Competing With

In Brazil, paying in installments isn't a credit product, it's just how people buy, and both halves of the market already had a way in. If you had a card, interest-free installments at checkout were the default, funded by the merchant: 6x, 10x, even 12x on everyday purchases. If you didn't, there was the carnê, the retailer's own booklet of monthly payment slips, the closest US cousin being store financing. Major retail chains like Casas Bahia lend against income to customers who often carry no formal credit mark at all.

And the cost of getting credit wrong in Brazil is brutal. Revolving credit card debt runs at over 400% a year, high enough that a 2024 federal law now caps total charges so a debt can no longer more than double. That was the bar we were entering against: two entrenched behaviors, and a regulatory environment where bad credit design lands hardest on the people who can least absorb it.

IF YOU HAD A CARD

0% interest

Interest-free installments at the checkout, funded by the merchants. The default way Brazil buys.

Checkout offers 6x, 10x, even 12x with no interest, on everyday purchases. No new credit check each time. The issuer already gave you the limit; you just need room in it.

The full amount hits that limit right away.

IF YOU DIDN’T

Crediário

The retailer’s own installment credit, paid with a booklet of monthly slips. Closest US cousin: store financing or rent-to-own.

The store’s own carnê. Pay in installments with no card at all, because the store underwrites you itself. Retailers like Casas Bahia lend even to people with no proof of income, and many of those customers already carry a credit mark.

It charges interest, but it’s still the door that opens.

Epilogue

Vivo later sunset the product, and I think that belongs in the story. My read on why is a positioning problem, not a demand problem. The card and the carnê both live at a checkout, attached to a purchase, with a seller absorbing risk because they want to close the sale. Parcela Pix had the customer relationship but no purchase to anchor to. It sat on the wrong shelf.

What the usage data made unmistakable is where the demand actually lives: person-to-person transfers inside informal support networks, the same underlying behavior that powers remittances worldwide. The product taught us exactly what should be built next. Sometimes evidence doesn't fix the current product. It points at the better one.